Polish banking sector leads Europe in digital adoption, with digital banking now a defining feature of the market as customers rapidly embraces mobile and online solutions. For example, in 2015 Poland has set its own successful mobile payment standard BLIK, which is currently responsible for 58% of all transactions in the country. Furthermore, local mobile banking adoption outpaces the West. Based on PKO BP Strategy 2025-2027 key features of the Polish banking system include a strong domestic deposit base and significant technological advancement. The sector includes a mix of private and state ownership, with state-controlled institutions managing nearly half of the sector's assets.

Poland ranks as the EU’s 6th largest economy, driving rapid tech investments amid cost pressures and regulations. According to EBA Work Programme for 2025, out of 64 European banks tested, Bank Pekao S.A took first place in the ranking, thanks to its highest resilience score and minimal CET1 decline. And although all together the Polish Banking Market is still a bit behind the European leaders like Germany, France, Netherlands, Sweden, and Italy, the country is on the right track to climb up the rankings in the nearest future. If the growth sustains a 5-7% GDP pace, Poland could lead Europe by 2030.

Top banking trends such as digital transformation, regulatory adaptation, and customer-centric innovation are critical for future growth. What role does IT Outsourcing play in this area? Let’s find out.

Market Overview of the Polish Banking

The Polish banking sector is characterized by a diverse structure, blending state-owned giants (which control approximately 45% of total assets) with private institutions, all underpinned by robust capitalization from domestic deposits. This stability is reinforced by the government's significant strategic ownership, particularly as Poland's loan portfolio has long been dominated by variable-rate products that expose banks to interest rate volatility. Complementing these major players are regional banks serving localized markets, alongside smaller institutions that often grapple with technological upgrades due to resource constraints, frequently resorting to hybrid or patchwork IT solutions. These dynamics are further shaped by ongoing consolidation, as international banks divest their Polish operations to streamline global footprints.

Amid this evolving landscape, banks are navigating transformative trends such as generative AI for customer personalization, hybrid cloud architectures, open banking under PSD3, and embedded finance integrations. The rapid rise of neobanks heightens competitive pressures, even as new regulatory frameworks (including CSRD for ESG disclosures and the EU AI Act) impose stricter compliance demands around data privacy, cybersecurity, and sustainability. These requirements, coupled with escalating costs from legacy system maintenance, intensify operational strains. Despite recent tailwinds from elevated interest rates that have driven return on equity (ROE) above 15-20% and record profitability, headwinds persist: net interest margin (NIM) compression of -71 basis points, wage inflation rising 7-20%, and unresolved FX mortgage risks continue to challenge resilience. With net interest income remaining as a cornerstone of revenue, yet highly sensitive to deposit and loan rate fluctuations, these pressures underscore the need for strategic adaptation to sustain long-term profitability.

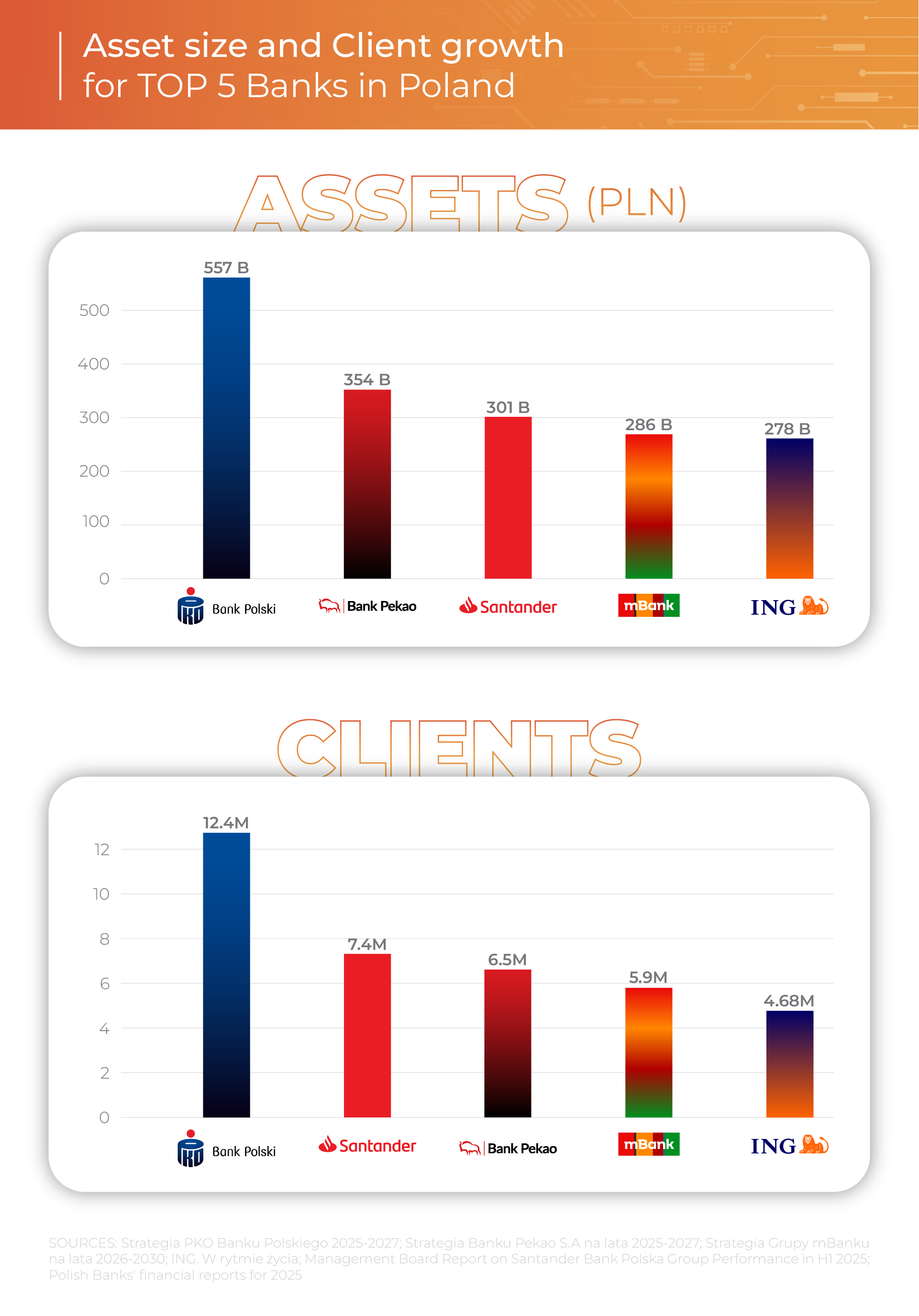

Top 5 Polish Banks in 2026

PKO BP, Pekao, Santander (Erste Group), mBank and ING Bank Śląski are considered leading banks in Poland, investing heavily in technology and innovation to enhance operational efficiency and maintain a competitive edge in the evolving banking landscape. They often collaborate or compete with other banks in the sector, shaping overall productivity and strategic direction within the Polish banking industry.

Key Characteristics of the 5 TOP banks in Poland

- Poland's largest bank by assets and clientele, positions itself as the undisputed market leader through its "Strategy for Growth," emphasizing seven pillars that leverage its scale to drive sustainable value. They rely heavily on client-centric universal model, spanning daily needs, financial futures, business financing, energy transition support, ecosystems, and international expansion, which is aimed at ROE of over 18% by 2027. Investments in engaging digital offerings, data platforms, and partnerships underscore its digital leadership, while prioritizing simple, secure tech and stable results differentiates it from peers. PKO's high maturity enables ecosystem plays and overseas growth, setting it apart from Pekao's domestic focus or Santander's efficiency drive.

- Upcoming challenges: Scaling tech infrastructure for over 15 million clients amid cyber and geopolitical risks demands advanced SRE and zero-trust security, without letting costs erode margins in a consolidating market.

- Built on Growth, Availability, and Efficiency, they focus on nine directions to solidify its position among Poland's most profitable banks, targeting ROE of over 18%, C/I over 35%, and CoR 65-75 bps by 2027. Pekao excels in client lifecycle support via PZU bancassurance synergies, integrated leasing/factoring, corporate sector growth, omnichannel access (conversational banking, optimized branches), and operational streamlining through data ecosystems and process ergonomics. This aspirational culture of simplicity, partnership, and responsibility marks its identity. Pekao bridges growth and efficiency more evenly than PKO's scale-focused ecosystems or Santander's remote emphasis, prioritizing bancassurance and micro-enterprise ties unique to its PZU ownership.

- Upcoming challenges: Balancing rapid retail and corporate expansion with low C/I amid tech catch-up requires disciplined automation and data integration, especially under resource constraints in a competitive field.

- Poland's digital pioneer and fourth largest by assets, mBank pursues a "Digital First" approach built on innovation, agility, customer obsession, and operational resilience. It targets ROE above 16% by 2027 through hyper-personalized digital experiences, AI-powered advisory (robo-advisors, predictive analytics), and seamless integration across retail, corporate, and investment banking. mBank stands out because it was one of the first to offer neobank features like partnerships for embedded finance, open banking APIs, and a highly-rated mobile app, all while keeping a small number of This tech-native DNA sets it apart from PKO's scale-driven ecosystems, Pekao's balanced omnichannel, and Santander's remote efficiency, positioning mBank as Poland's fintech challenger with pan-European ambitions via its Commerzbank ties.

- Upcoming challenges: Accelerating corporate digital adoption amid legacy migration risks requires robust API ecosystems and cloud-native scalability, while defending market share against pure neobanks demands continuous UX innovation without inflating tech spend.

- Ranking fifth, ING Bank Śląski leverages its global ING heritage for a progress-oriented strategy emphasizing sustainable growth, digital mastery, and ecosystem orchestration, aiming for a ROE of 15–17% and a C/I under 40% by 2027. Core pillars include hyperconnected banking (Moje ING app with 5M+ users), green financing leadership (ESG-linked loans), and SME empowerment via integrated payroll/tax platforms. ING excels in proactive customer engagement through behavioural data insights, contactless ecosystems, and international payment rails, blending Dutch efficiency with local Silesian roots. It contrasts PKO/Pekao's domestic scale, Santander's cyber focus, and mBank's neobank edge by prioritizing sustainable, cross-border innovation and regulatory foresight.

- Upcoming challenges: Deepening SME penetration in a consolidating market while navigating DORA cybersecurity mandates calls for advanced regtech and AI governance, alongside balancing green ambitions with profitability in volatile energy transition financing.

Santander (now Erste Group)

- The bank emphasizes remote-first efficiency in its group strategy, prioritizing mobile app enhancements, RPA-driven process simplification, and a cybersecurity-centric culture to maintain top DSPW (digital services) rankings despite network optimization. Sustainable development focus, automation for cost control, and robust antifraud measures, position it as an agile international player in Poland's market. Santander stands out with its cyber and remote emphasis and branch rationalization, contrasting PKO's expansive ecosystems and Pekao's omnichannel/bancassurance balance, reflecting its global group's efficiency mandate.

- Ownership Change to Erste Group: In May 2025, Santander announced the sale of approximately 49% of Santander Bank Polska's share capital to Erste Group for €6.8 billion (PLN 584 per share), plus 50% of its Polish asset management arm (Santander TFI) for €0.2 billion, totaling €7 billion. The deal closed in January 2026 after regulatory approvals, making Erste the largest shareholder with de facto control (board nomination rights) and full financial consolidation. On March 31, 2026, an EGM approved rebranding to Erste Bank Polska (effective Q2 2026), unifying Erste's CEE identity; Santander Consumer Bank remains separate under Santander Group (9.7% stake post-sale).

- Upcoming challenges: Navigating CHF mortgage litigation and rate volatility demands precise risk modelling and legal tech, while sustaining digital leadership requires ongoing RPA/AI investments amid regulatory scrutiny.

It is important to note that banks are expected to adopt compliance technologies that automate regulatory reporting to stay agile in a rapidly changing landscape.

To remain competitive in this dynamic environment, financial institutions must continue to invest in emerging technologies and adapt their strategies to meet evolving customer expectations. By doing so, they can strengthen their position in the capital markets, deliver superior investment advice, and build lasting relationships with clients seeking smarter financial choices.

Banking Trends in Polish market

Polish banks offer advanced mobile apps and fast, real-time transfers, enhancing consumer convenience. Real-time payments (RTP) will become the norm, allowing businesses and individuals to send and receive money instantly, 24/7. The payment landscape is evolving, with consumers expecting smarter, more convenient payment options. Physical branches will remain essential as trust anchors, but their role will evolve to blend human connection with AI-driven convenience. Banks must modernize their core systems to enable smart money, including the integration of blockchain and distributed ledger technologies. Modern institutions all prioritize digital-first hybrid models, as PKO Strategy mentions.

What other practices, functionalities, and innovations are emerging in the banking industry?

- Superior Mobile and Omnichannel Experiences - Polish banks are achieving mobile NPS over 70 through intuitive apps like mBank's redesigned CompanyMobile, which blends user engagement with practical utility for seamless corporate banking. These omnichannel strategies effectively serve seniors through trusted branch interactions while delivering digital excellence to tech-savvy users, consistently hitting customer effort scores above 90. Together, this approach drives customer loyalty and enables ecosystem expansion, solidifying market leadership for forward-thinking institutions.

- Automation Driving Operational Efficiency - Generative AI is streamlining document processing and call center operations, which enables smarter and more secure transaction handling across banking functions. These automation tools help reallocate resources toward strategic innovation even amid rising wage pressures, while algorithmic trading platforms enhance capital market efficiency. The result is a leaner cost structure that sustains profitability in competitive environments.

- AI/ML at Risk and Personalization Core - AI/ML technologies are enhancing credit scoring accuracy and real-time fraud detection, building on data analytics that refine underwriting processes and CRM personalization for lasting competitive advantage. Such integration proves essential for maintaining ROE resilience, as predictive models consistently outperform legacy systems in volatile conditions. This foundational capability ultimately differentiates banks navigating Poland's dynamic risk landscape.

- Cloud Modernization for Scalability - Azure and GCP hybrid deployments are replatforming legacy cores to cut costs while ensuring compliance and scalability for high-volume BLIK transactions. Cloud-native architectures efficiently handle over 15 million clients without proportional expense growth, and their seamless PSD3 API support accelerates open banking adoption. These modernization efforts represent strategic investments that future-proof operations for sustained growth.

- Regulatory and ESG Compliance - PSD3, ISO 20022, and CSRD requirements are driving sophisticated ESG and climate risk modeling, complemented by DORA/NIS2 cyber mandates that demand robust resilience frameworks. Banks are building integrated governance structures that transform compliance from a cost center into a strategic differentiator, as exemplified by Santander's navigation of complex legal and environmental challenges. Quantitative audit tools further ensure these frameworks enable secure, innovative service delivery.

- Real-Time Payments and Smart Money - ISO 20022 standards combined with BLIK are powering AI-routed instant payments and stablecoin pilots, revolutionizing transaction speed and flexibility. Digital wallets, as Capgemini emphasizes, are reshaping liquidity management for both consumers and businesses through always-available access. Core system upgrades thus become essential for Polish banks to secure Central and Eastern European leadership, supporting 24/7 operations that ultimately boost transaction volumes and revenue potential.

Customer Experience and Satisfaction in Financial Institutions

Customer experience and satisfaction have become critical drivers of success, with evolving customer expectations reshaping how financial institutions deliver banking services. As more customers seek seamless, personalized interactions across digital channels, banks are investing heavily in digital transformation and leveraging data analytics to better understand and anticipate client needs.

The integration of AI and machine learning enables banks to personalize offerings, streamline banking operations, and enhance risk management, resulting in improved operational efficiency and higher customer satisfaction.

Implications for Banking Industry

Regulatory changes are driving banks to invest in systems that track and report on their ESG-related activities due to tightening disclosure requirements. A breach or failure to meet privacy standards can severely damage a bank's reputation and customer trust, making heavy investment in cybersecurity critical. The rapid pace of emerging threats demands a more integrated, real-time approach to risk management, and investing in tools and infrastructure to combat cyber threats is likely to increase as threats evolve.

On a different note, Poland’s population is shrinking and rapidly aging, with a steadily declining share of young people under 35, which reduces the pool of future active banking customers. Digitalization, therefore, becomes less about cost‑cutting alone and more about securing long-term relationships with the smaller, but crucial, cohort of younger customers. For many institutions, the risk of demographic decline means that digital transformation is now a strategic necessity, not an option, if they want to maintain customer growth and market share.

Digital shifts reshape operations and competition:

- Efficiency Gains - Legacy systems (over 20 years old in about half of Polish banks) are a major cost drain. Switching to cloud and AI solutions, including RPA, real-time analytics, and automation, can cut these costs by 15-30%. While net interest income drives profitability, it’s sensitive to deposit and loan rate changes. NPLs remain low at under 5%, but FX risks call for advanced ML early-warning systems.

- Customer Shift - Hybrid models balance the needs of seniors (64% prefer branches) and tech-savvy users (mobile NPS >70%). Banking’s future depends on seamless experiences across digital and physical channels. BLIK powers 53% of transactions, while ecosystems like PKO-Allegro fuel over 10% client growth.

- Revenue Diversification - Embedded finance, SME platforms, and AI agents open new revenue streams like merchant lending - outpacing neobanks. AI-driven data analytics now powers personalized financial planning, from custom savings plans to tailored investment advice.

- Risks - Cyber threats like DDoS and AI attacks, plus ESG compliance, are pushing IT spending up 20-40%. Banks ignoring these lose ground to fintechs. Cybersecurity demands AI threat detection and multi-factor authentication, while privacy rules require stronger data protection and transparency.

TOP 3 IT Outsourcing Challenges and Opportunities

- Talent Shortages in AI and Cybersecurity - Polish banks like PKO BP and mBank face severe gaps in AI/ML engineers and cybersecurity pros, with demand outpacing supply by 25% amid PSD3 and AI Act rollout. Internal teams can't handle gen AI for personalization or 24/7 threat monitoring, delaying projects. NATEK supplies 50-80 FTE Specialists via Staff Augmentation and T&M pilots for MLOps/SIEM, enabling rapid AI agent deployment and cyber defenses.

- AI Act, CSRD & KNF Compliance - EU AI Act and CSRD hit Polish banks hard, requiring AI audits, ESG disclosures, and KNF reporting, straining teams amid FX mortgage provisions and climate risk mandates, with fines up to 4% revenue. NATEK builds ESG data lakes and compliance tools with 3-6 week ROI pilots, handling PSD3 transitions for banks, ensuring seamless KNF audits and innovation focus.

- Cyber Threats Amid Geopolitical Risks - Polish banks face escalating cyber-attacks (like AI-powered DDoS floods, deepfake fraud, and ransomware) that exploit hybrid cloud setups and geopolitical tensions (for example hybrid warfare from state actors). Last year, CERT Poland logged around 19,000 incidents against finance, with breaches costing millions and 99% of cloud failures tied to misconfigurations. As NATEK we deliver fixed-price SIEM/SOAR platforms and Zero Trust architectures to secure critical systems like BLIK payments and real-time transfers. Our banking-proven track record ensures KNF-compliant protection, rapid threat response, and zero-downtime resilience, keeping our Customers' operations safe while meeting regulatory deadlines.

Take your bank to a new level of innovation with NATEK Team

As NATEK, one of the most recognized organizations among top IT providers for finance, we support banks in bringing to life new trends, strategies and innovations thanks to our services. Our cloud migrations, AI platforms, RPA automation, and cybersecurity, deliver 15-30% savings via FinOps and MLOps. Find out more about services or contact us now for more information.

You can also inform us about your needs and expectations through direct contact with NATEK Sales Prospection Team Lead Andrzej Osman on LinkedIn or at andrzej.osman@natek.eu, and #growITwithus!